Digital marketplaces were built for scale. Vendors get onboarded in minutes, supply grows quickly, and transactions occur instantly between buyers and sellers.

But these same characteristics that make marketplaces so successful also make them attractive targets for organized document fraud.

Or, more specifically: serial fraud.

Instead of forging one document for a single application, criminals create marketplace document fraud using editable templates and automations that can create thousands of fraudulent submissions with minor changes to the documents (names, addresses, or transaction details etc).

The result is a new form of fraud that behaves less like individual deception and more like an automated campaign.

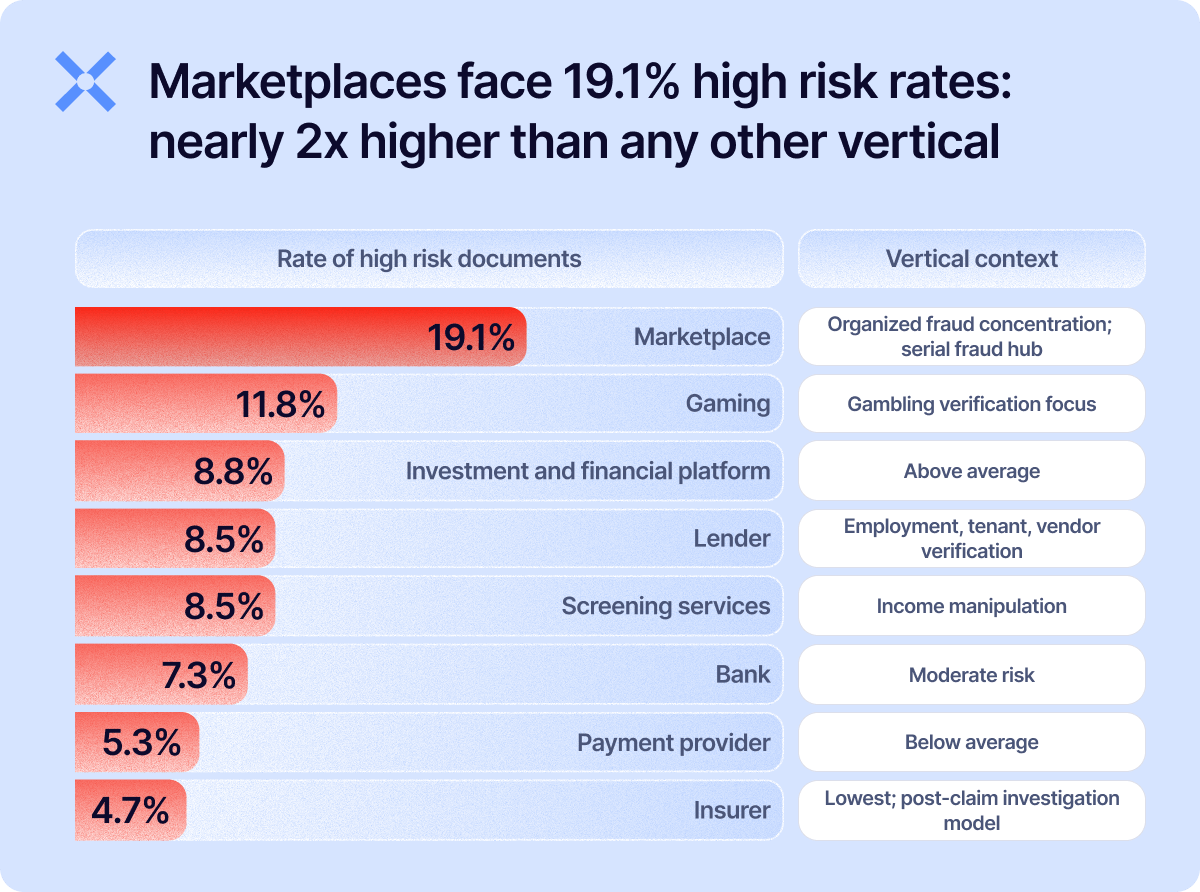

Our analysis of 170 million+ documents revealed that serial fraud increased sevenfold from 2024 to 2025, with the vast majority concentrated in marketplace environments. This could be the reason for their absurdly high rate of high-risk documents: 19.1% (almost double any other vertical).

This isn’t an accident. Marketplaces combine the exact operational features that large-scale fraud campaigns thrive on.

Marketplaces create the perfect operating environment

Large marketplaces process huge numbers of vendor applications, often across multiple regions and verticals. They also grow at the speed of their vendor onboarding process. Long onboarding delays discourage legitimate sellers, so platforms naturally optimize their processes for efficiency.

Some of the vulnerabilities marketplaces experience include:

Size and scale

In most places, it’s not difficult to open a legitimate business. With modern editing and AI tools, it’s even easier to create a fake one. The natural volume of legitimate businesses a marketplace can support is massive. Fraudsters can take advantage of this flood of data and evade detection through the noise of so many people onboarding.

Risk tolerance vs growth

Their inherent desire to onboard as many “good” vendors as possible makes for a difficult balance between user experience and risk tolerance. Too tight and they lose business, too loose and they allow fraudsters to enter.

Variety of document types

Businesses and individuals may use any number of document types to onboard. Identity documents, business licenses, tax forms, regulatory reviews, etc… These all vary in layout, complexity, language, and unique distinguishing characteristics, putting potential burden on marketplace onboarding specialists.

Once approved, vendor accounts can immediately process payments, sell goods, and interact with customers.

That combination of rapid onboarding and instant financial access makes marketplace accounts extremely valuable and accessible to fraudsters.

This is what makes marketplaces especially susceptible to serial fraud, where we find 86% of overall serial fraud instances.

The overlooked attack surface: KYB

Fraud discussions often focus on customer identity verification, but marketplace ecosystems rely just as heavily on verifying the legitimacy of the businesses that operate on the platform.

Data from our document fraud report highlighted this risk:

- Broader KYB verification processes show high-risk signals in 12.5% of their documents.

Fake invoices, altered business licenses, and manipulated incorporation documents can all be used to establish a presence on a platform before fraud begins. But the nature of these documents makes them vulnerable to fraud.

To illustrate this, let’s look at two of the most common documents used for vendor onboarding: invoices and business licenses.

Invoices

Invoices vary significantly because they’re not always from a consistent originating entity. Anyone can create an invoice in a Word document that might be acceptable for a small business or individual contract. The inherent variability in legitimate construction methodologies, in addition to wildly different layouts and content, make identifying anomalies especially difficult.

Business licenses

Business licenses format also vary significantly, not only internationally, but even regionally within a country. Many users also still have these documents as physical artifacts. This means they are required to digitize the documents themselves (scanner, phone camera capture, etc…) and sometimes transform it again (such as in a PDF).

Moving away from an original digital document increases the risk of intentional manipulation being obscured as the document is (effectively) recreated as a new digital document. We call this “format hopping.”

In contrast, documents for other verticals (such as tenant screening) can be more focused and related to known originators.

Bank statements and utility bills, supporting proof of income and proof of address requirements, tend to be available digitally and generated from known entities. The more common or recurring nature of these documents increases the opportunity to identify anomalies.

From fake documents to reusable fraud infrastructure

What makes serial fraud particularly dangerous is the way it transforms documents into reusable assets.

Instead of generating each fraudulent document from scratch, criminals produce templates that can be modified and resubmitted across many platforms. In some situations they even publish these document fraud templates onto template farms or template hubs (places they can be bought and downloaded by anyone).

Small details are changed to avoid simple duplication checks, but the underlying document structure remains the same. In some cases, a single document template has been used to generate applications rapidly. We’ve seen the same bank statement template used thousands of times across different clients.

But the infrastructure doesn’t stop there. Document generators pose an ever present threat as well, not to mention the ever-improving capabilities of the latest AI-image generation technology.

In the most threatening of these cases, these documents are packaged together to onboard entirely fake accounts onto various platforms, which are then sold to the highest bidder.

This approach fundamentally changes the nature of document fraud. It is no longer a question of identifying a single fake document. Instead, organizations are dealing with coordinated campaigns built around reusable fraud infrastructure.

The solution: AI document fraud detection

At Resistant AI, we specialize in serial fraud identification, spotting signals like recurring document templates across vendors, but also numerous submissions from the same vendor.

In some cases, fraudsters get rejected initially, but make changes (either to the raw document or how they’re submitting it) and resubmit over and over, in an attempt to slip under a client’s risk threshold. That’s why indicators that spot these multiple attempts are essential.

Adaptability is another hurdle to cross. The ability to align a detection strategy to business risk preferences is critical.

The ability to make changes is critical. Organizations can completely change their corporate policies for any number of reasons, both internal and regulatory. We’re able to adapt to realign our solution for their needs.

Interestingly, sometimes an organization's standard business processes are causing the vulnerability.

It’s important to understand that the solution needs to be adaptable not just to business needs/expectations, but also evolving tactics. Fraudsters change behavior patterns and thus solutions need to be flexible enough to adapt on the fly.

Resistant AI can also augment its models with additional signals tailored to specific fraud vectors observed within a client’s ecosystem.

Conclusion

For marketplaces, there’s a clear action plan:

Serial fraud campaigns exploit the limits of this approach. Each submission may appear slightly different, even though all of them originate from the same underlying template.

The real signal often emerges only when submissions are compared collectively rather than individually.

Resistant Documents forensically analyzes documents to determine if they’re trustworthy. By combining document fraud detection with behavioral data and device fingerprinting, we’re able to help organizations detect up to 30% more fraud than if you’re just looking at the document by themselves.

Scroll down to book a demo.

Fraud awareness, examples, and lessons

Learn more about fraud in specific industries, best practices, and targeted documents.

View all

Key takeaways Risk appetite defined. Risk appetite is the level of fraud and financial crime risk an organization ...

PRAGUE – 22 July 2026 – Resistant AI, a leading provider of document fraud detection solutions, today announced ...

In our last article, we teased that Fakedocshop, a popular document template farm running on subscriptions, has ...

Fake New York business licenses are risky in 2026. Whether it’s to provide jurisdictional privileges, or renew the ...

When we think about APP fraud, our hearts go out to the victims. But in 2026, banks in the UK are shouldering a ...

If you've seen as many template farm websites as we have, things start to blur. Hundreds of sites are selling ...